Turkish lira: Another crisis unfolds

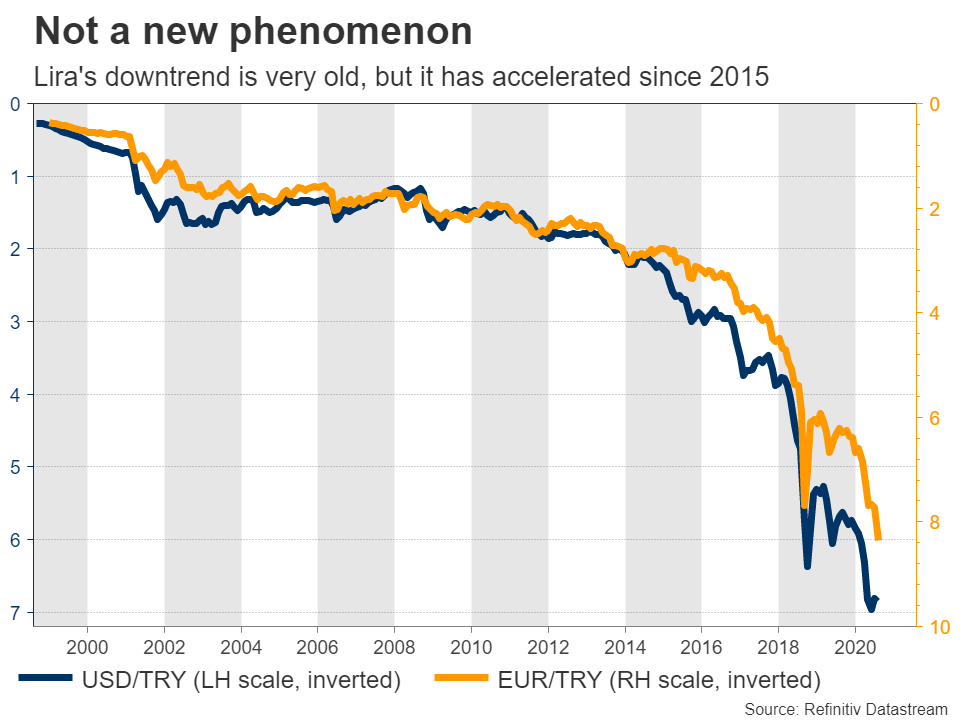

The past few years have been a difficult period for the Turkish currency, and things have unfortunately not calmed down in 2020. The lira hit an all-time low against the dollar in May, then against the euro in July, and then plunged to fresh record lows against both currencies this week.

This is not a new phenomenon. The lira has been in a broader downtrend for two decades now, though the pace of the currency’s collapse has accelerated in recent years as a cocktail of worrisome economic developments has caused capital to flee the country.

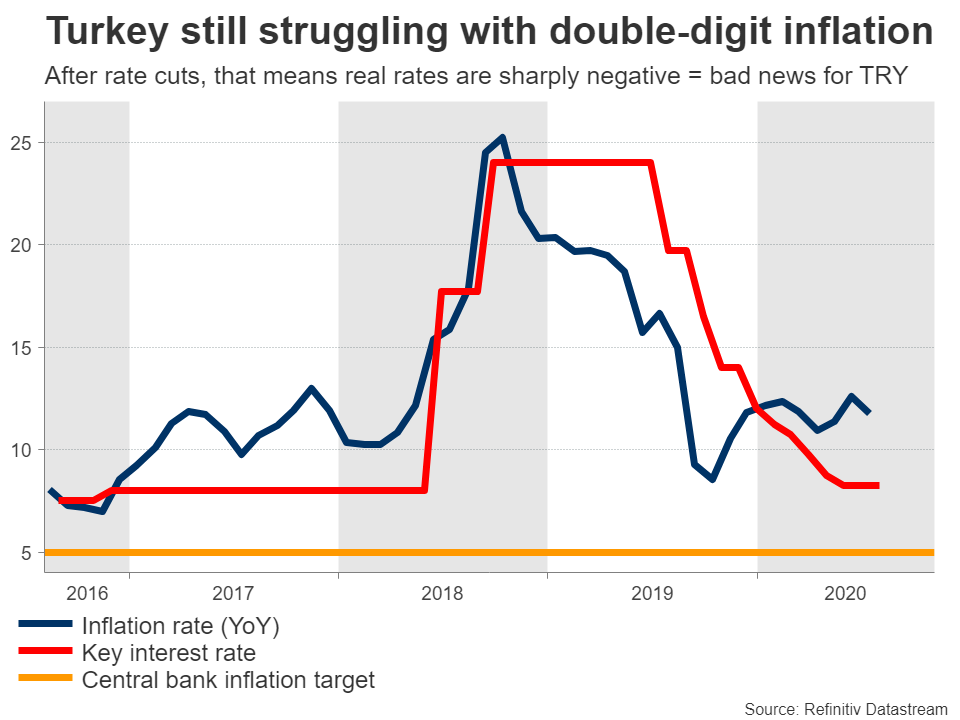

Inflation soars, deficits widenThe main issue that has devastated the lira is double-digit inflation. High inflation erodes purchasing power and is anathema for currencies. Even after the pandemic, when inflation would naturally sink because of lower demand, Turkey’s inflation rate still clocked in at almost 12% in July – more than double the 5% targeted by the central bank.

To make matters worse, Turkey also runs a chronic current account deficit. That basically means the nation is a net borrower, importing more than it exports and relying on capital flows from abroad to finance the difference. The problem is that if these capital flows dry up or foreign investors decide to withdraw their investments, this begins to exert massive downward pressure on the currency.

Additionally, both the government and the private sector have high levels of debt in foreign currencies, which become much harder to pay back with a depreciating lira.

Central bank prioritizes growthIn a situation like this, the central bank would typically raise interest rates to rein in inflation, stabilize the current account deficit by attracting more foreign capital, and defend the currency. Of course, this is a painful process. Higher rates would slow down borrowing, hit demand, hurt economic growth, and even risk an increase in unemployment.

Even though the central bank did raise rates dramatically in 2018 to avert a full-blown currency crisis, it has since lowered them again by more than 15 percentage points, to 8.25% currently. That’s a tricky endeavor. It’s basically a gamble, where policymakers are trying to boost growth at all costs, by incentivizing another borrowing boom and allowing inflation to soar.

The gamble is whether their FX reserves will be sufficient to keep the lira from collapsing while they attempt to boost growth. Foreign reserves naturally run out when you are constantly trying to defend a currency, and Turkey has been burning through its own at a furious pace.

What’s the point of all this? Since inflation exceeds interest rates so dramatically, Turkey has some of the most negative real interest rates globally, which is really bad news for a currency over time. Why would foreign investors put capital into a Turkish bank, where they might earn 9% interest, when inflation is running at 12%? That implies a loss of 3% per year, which is unlikely to attract foreign capital, and if anything, might push investors to leave Turkey altogether.

What can be done?In the short term, there are two methods that could halt the lira’s slide, but admittedly, neither is likely to be implemented.

The first would be to raise interest rates again. But the central bank doesn’t want to do that. We are in the middle of a crisis, which will naturally hurt the economy, so their main priority is to stimulate growth at all costs, even if that means higher inflation and a weaker currency. Plus, there may be some political pressure involved, as President Erdogan has long been a critic of high interest rates, even describing them as “the mother and father of all evil”.

The second would be introducing strict capital controls. It looks bad, as it tarnishes an economy’s credibility and might incite panic among foreign investors, but if you are trying to stop a currency crisis, it works. That option however has been repeatedly ruled out by the nation’s finance minister, who is also President Erdogan’s son-in-law.

What’s most likely then?In a nutshell, the lira will likely be allowed to depreciate. The central bank has already burned through most of its FX reserves, and lately, it has been spending reserves it has borrowed from local banks to support the currency. It has also resorted to more ‘questionable’ methods, such as making it more difficult to short the lira in the markets.

But these tools look exhausted. The lira wouldn’t be hitting new record lows against a US dollar that is weak itself, if they were effective. So it’s either rate hikes, capital controls, or allowing the currency to depreciate further. A currency can’t resist economic gravity for long.

At some point, the central bank will probably be forced to raise rates. But for that to happen, the lira probably has to experience more pain first, leaving policymakers no choice.

Beyond the lira – mind European banks and the euroIn the bigger picture, if Turkey indeed faces a new currency crisis, that could also be bad news for the euro. European banks are exposed to Turkey, much more than American banks, and if the situation worsens they might have to take losses on those operations.

The European banking system is still tormented by the legacy of the euro crisis, and with the pandemic likely to cause another spike in non-performing loans, any Turkey-related worries may spill over into the euro. Of course, this is a minor factor, but it may play some role in slowing down the recent uptrend in euro/dollar.免责声明: XM Group仅提供在线交易平台的执行服务和访问权限,并允许个人查看和/或使用网站或网站所提供的内容,但无意进行任何更改或扩展,也不会更改或扩展其服务和访问权限。所有访问和使用权限,将受下列条款与条例约束:(i) 条款与条例;(ii) 风险提示;以及(iii) 完整免责声明。请注意,网站所提供的所有讯息,仅限一般资讯用途。此外,XM所有在线交易平台的内容并不构成,也不能被用于任何未经授权的金融市场交易邀约和/或邀请。金融市场交易对于您的投资资本含有重大风险。

所有在线交易平台所发布的资料,仅适用于教育/资讯类用途,不包含也不应被视为用于金融、投资税或交易相关咨询和建议,或是交易价格纪录,或是任何金融商品或非应邀途径的金融相关优惠的交易邀约或邀请。

本网站上由XM和第三方供应商所提供的所有内容,包括意见、新闻、研究、分析、价格、其他资讯和第三方网站链接,皆保持不变,并作为一般市场评论所提供,而非投资性建议。所有在线交易平台所发布的资料,仅适用于教育/资讯类用途,不包含也不应被视为适用于金融、投资税或交易相关咨询和建议,或是交易价格纪录,或是任何金融商品或非应邀途径的金融相关优惠的交易邀约或邀请。请确保您已阅读并完全理解,XM非独立投资研究提示和风险提示相关资讯,更多详情请点击 这里。