XM市场研究

Week Ahead – Focus on US retail sales as debt ceiling drama rumbles on

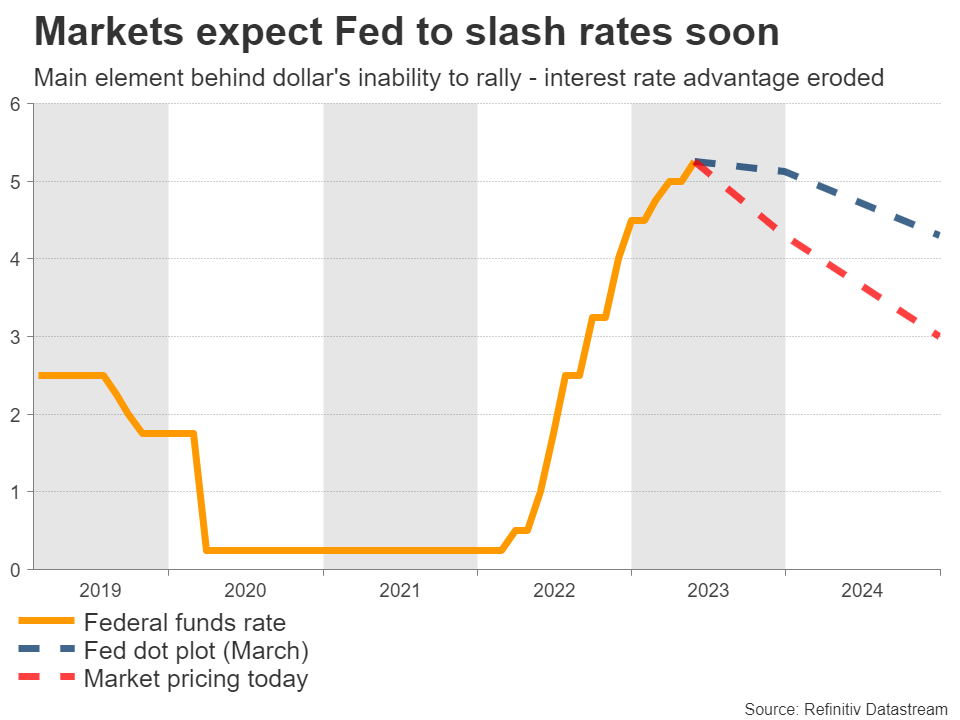

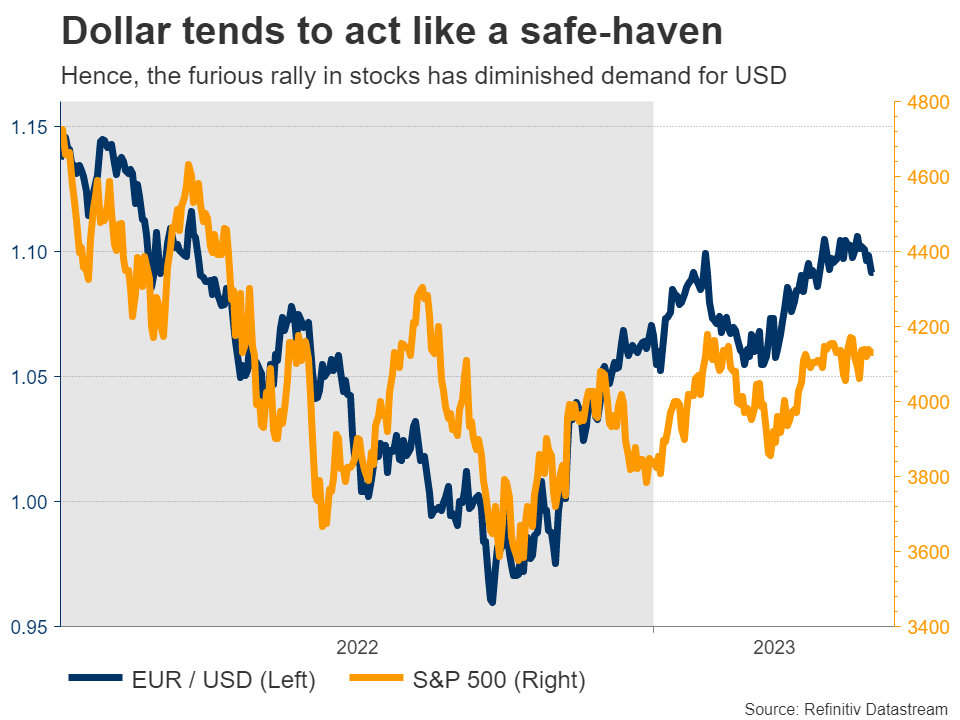

With no central bank decisions on the menu next week, investors will turn to data releases. Top of the list is the US retail sales report, which will help shape expectations about the Fed’s rate path, driving the dollar accordingly. There is also an onslaught of economic data from most major economies to keep traders busy, alongside an election in Turkey and the ongoing drama around the US debt ceiling. Can the dollar shake off the blues? It’s been a rough year for the dollar so far. Despite mounting signs that the US economy has regained momentum, the greenback has been trading ‘heavy’, struggling to sustain any upward momentum. Most rallies get rejected quickly, even if they are backed up by stronger data. Behind this sluggishness lies speculation that the Fed is about to start cutting interest rates soon. Markets expect the Fed to slash rates three times later this year in 25bps increments, starting in September. This is striking considering that core inflation seems sticky around 5.5%, way above its target.  Traders seem to be betting that the problems in the banking system will override inflation concerns, forcing the Fed to reduce borrowing costs in order to avoid a domino of bank failures, even if that means tolerating a period of higher inflation. Another problem for the dollar has been the rally in stocks. Since the greenback often acts like a haven asset, the optimistic tone in markets has limited demand for the reserve currency. The charts tell the same story - the dollar index topped in late September, right before the stock market bottomed. In other words, the dollar’s yield advantage has been eroded because of rate-cut bets, and its safe-haven qualities are not very popular right now. Therefore, for the greenback to start ‘working’ again, it might need an equity selloff that fuels demand for protection or a stream of encouraging data that dispels speculation of imminent rate cuts.

Traders seem to be betting that the problems in the banking system will override inflation concerns, forcing the Fed to reduce borrowing costs in order to avoid a domino of bank failures, even if that means tolerating a period of higher inflation. Another problem for the dollar has been the rally in stocks. Since the greenback often acts like a haven asset, the optimistic tone in markets has limited demand for the reserve currency. The charts tell the same story - the dollar index topped in late September, right before the stock market bottomed. In other words, the dollar’s yield advantage has been eroded because of rate-cut bets, and its safe-haven qualities are not very popular right now. Therefore, for the greenback to start ‘working’ again, it might need an equity selloff that fuels demand for protection or a stream of encouraging data that dispels speculation of imminent rate cuts.  This puts extra emphasis on US retail sales out on Tuesday, which will reveal how consumers are holding up. Forecasts point to a 0.7% monthly increase in April, a rebound following a decline of similar size last month. This notion is supported by an increase in Visa’s US Spending Momentum Index, yet similar card data from Bank of America point to a spending rise of just 0.3% in April, presenting some downside risks. Meanwhile, debt ceiling negotiations will continue. The Treasury Secretary has warned the US could face default by early June without a deal, although in reality, it is likely closer to July. Outside of short-term Treasury yields and credit default swaps, markets haven’t cared much about this standoff so far, but that might change as the X-date draws closer. China and Japan await key dataCrossing into China, the ball will get rolling on Tuesday with retail sales, industrial production, and fixed asset investment - all for April. Investors will be looking at whether the reopening momentum has started to fade, as recent business surveys suggested. Over in Japan, things will heat up with GDP growth data for Q1 on Wednesday, ahead of the latest round of inflation stats on Friday. The Japanese economy is expected to have grown again entering 2023, albeit just barely.

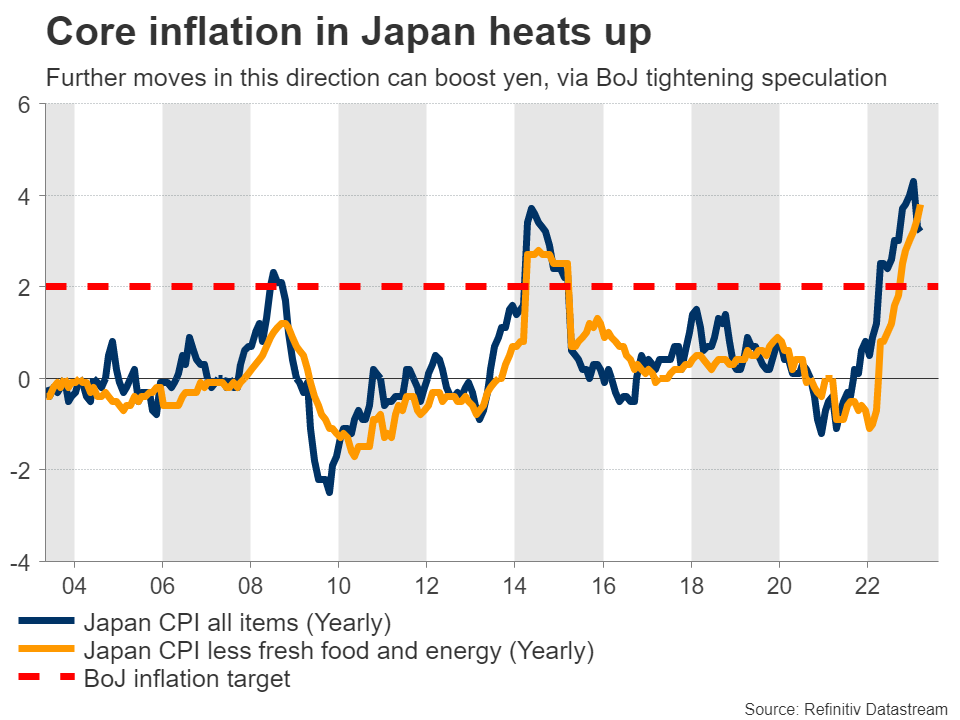

This puts extra emphasis on US retail sales out on Tuesday, which will reveal how consumers are holding up. Forecasts point to a 0.7% monthly increase in April, a rebound following a decline of similar size last month. This notion is supported by an increase in Visa’s US Spending Momentum Index, yet similar card data from Bank of America point to a spending rise of just 0.3% in April, presenting some downside risks. Meanwhile, debt ceiling negotiations will continue. The Treasury Secretary has warned the US could face default by early June without a deal, although in reality, it is likely closer to July. Outside of short-term Treasury yields and credit default swaps, markets haven’t cared much about this standoff so far, but that might change as the X-date draws closer. China and Japan await key dataCrossing into China, the ball will get rolling on Tuesday with retail sales, industrial production, and fixed asset investment - all for April. Investors will be looking at whether the reopening momentum has started to fade, as recent business surveys suggested. Over in Japan, things will heat up with GDP growth data for Q1 on Wednesday, ahead of the latest round of inflation stats on Friday. The Japanese economy is expected to have grown again entering 2023, albeit just barely.  On the inflation front, inflationary pressures probably continued to heat up in April, mirroring the forward-looking Tokyo CPIs. That would be pleasant news for the Bank of Japan, possibly fueling speculation for policy tightening in the future, perhaps this summer already. The BoJ’s reluctance to tighten policy has devastated the yen, so any hints that this might change can help the currency regain strength. Governor Ueda has signaled he’s open to tightening, provided that inflation is persistent. For the yen, the dream scenario would be for the BoJ to start tightening right as other central banks stop, during a period of turbulence in global markets.Risk-linked currencies eyed, Turkey goes to electionsTurning to currencies with strong links to risk sentiment, the British pound will be in the spotlight Tuesday with the release of jobs data for March. The Bank of England disappointed traders this week by not providing any strong clues about future action, so markets are pricing the rate decision next month almost like a coin toss. In Australia, there’s a barrage of releases starting on Tuesday with the minutes of the latest RBA meeting, where the central bank unexpectedly raised interest rates. The wage price index for Q1 will follow Wednesday, ahead of jobs numbers for April on Thursday. Over in Canada, the latest inflation stats are out Tuesday, ahead of retail sales on Friday. Market pricing suggests the Bank of Canada is done raising rates, so anything that challenges this perception could inject more volatility into the Canadian dollar, which has been shaken around lately by massive swings in oil prices.

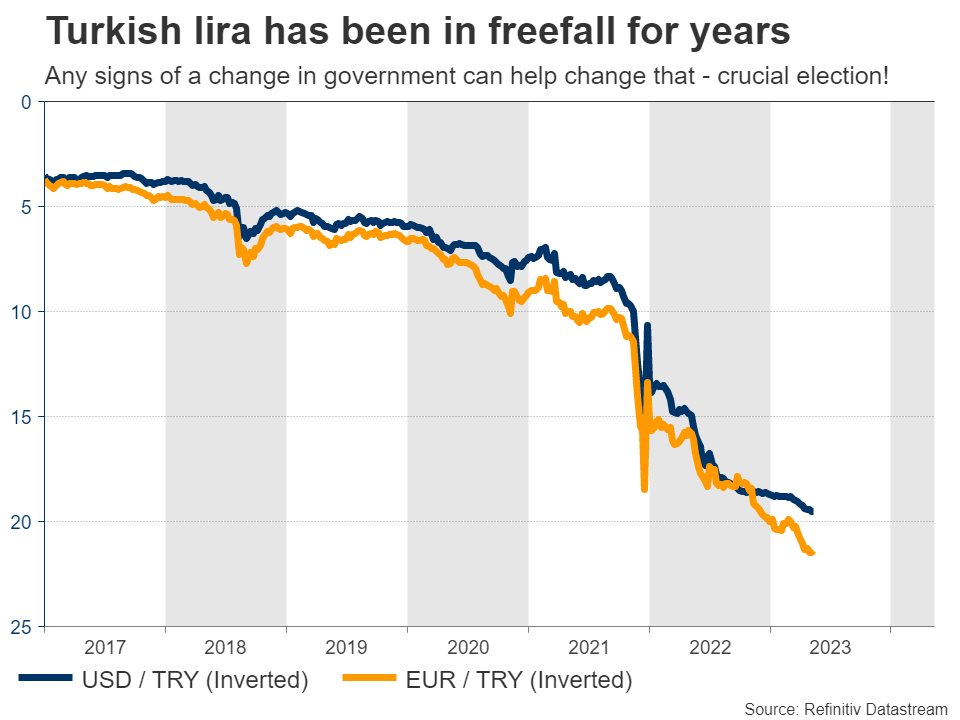

On the inflation front, inflationary pressures probably continued to heat up in April, mirroring the forward-looking Tokyo CPIs. That would be pleasant news for the Bank of Japan, possibly fueling speculation for policy tightening in the future, perhaps this summer already. The BoJ’s reluctance to tighten policy has devastated the yen, so any hints that this might change can help the currency regain strength. Governor Ueda has signaled he’s open to tightening, provided that inflation is persistent. For the yen, the dream scenario would be for the BoJ to start tightening right as other central banks stop, during a period of turbulence in global markets.Risk-linked currencies eyed, Turkey goes to electionsTurning to currencies with strong links to risk sentiment, the British pound will be in the spotlight Tuesday with the release of jobs data for March. The Bank of England disappointed traders this week by not providing any strong clues about future action, so markets are pricing the rate decision next month almost like a coin toss. In Australia, there’s a barrage of releases starting on Tuesday with the minutes of the latest RBA meeting, where the central bank unexpectedly raised interest rates. The wage price index for Q1 will follow Wednesday, ahead of jobs numbers for April on Thursday. Over in Canada, the latest inflation stats are out Tuesday, ahead of retail sales on Friday. Market pricing suggests the Bank of Canada is done raising rates, so anything that challenges this perception could inject more volatility into the Canadian dollar, which has been shaken around lately by massive swings in oil prices.  Finally in Turkey, the nation will elect its next parliament and president on Sunday. President Erdogan is lagging behind his main rival Kilicdaroglu, although neither candidate is expected to secure 50% of the votes, which means there will probably be a second round in two weeks. A strong showing by Kilicdaroglu could help the Turkish lira to appreciate, perhaps with a large gap at the open on Monday, on expectations that a new government will restore orthodox economic policies and allow the central bank to raise interest rates in order to fight runaway inflation.

Finally in Turkey, the nation will elect its next parliament and president on Sunday. President Erdogan is lagging behind his main rival Kilicdaroglu, although neither candidate is expected to secure 50% of the votes, which means there will probably be a second round in two weeks. A strong showing by Kilicdaroglu could help the Turkish lira to appreciate, perhaps with a large gap at the open on Monday, on expectations that a new government will restore orthodox economic policies and allow the central bank to raise interest rates in order to fight runaway inflation.

Traders seem to be betting that the problems in the banking system will override inflation concerns, forcing the Fed to reduce borrowing costs in order to avoid a domino of bank failures, even if that means tolerating a period of higher inflation. Another problem for the dollar has been the rally in stocks. Since the greenback often acts like a haven asset, the optimistic tone in markets has limited demand for the reserve currency. The charts tell the same story - the dollar index topped in late September, right before the stock market bottomed. In other words, the dollar’s yield advantage has been eroded because of rate-cut bets, and its safe-haven qualities are not very popular right now. Therefore, for the greenback to start ‘working’ again, it might need an equity selloff that fuels demand for protection or a stream of encouraging data that dispels speculation of imminent rate cuts. This puts extra emphasis on US retail sales out on Tuesday, which will reveal how consumers are holding up. Forecasts point to a 0.7% monthly increase in April, a rebound following a decline of similar size last month. This notion is supported by an increase in Visa’s US Spending Momentum Index, yet similar card data from Bank of America point to a spending rise of just 0.3% in April, presenting some downside risks. Meanwhile, debt ceiling negotiations will continue. The Treasury Secretary has warned the US could face default by early June without a deal, although in reality, it is likely closer to July. Outside of short-term Treasury yields and credit default swaps, markets haven’t cared much about this standoff so far, but that might change as the X-date draws closer. China and Japan await key dataCrossing into China, the ball will get rolling on Tuesday with retail sales, industrial production, and fixed asset investment - all for April. Investors will be looking at whether the reopening momentum has started to fade, as recent business surveys suggested. Over in Japan, things will heat up with GDP growth data for Q1 on Wednesday, ahead of the latest round of inflation stats on Friday. The Japanese economy is expected to have grown again entering 2023, albeit just barely. On the inflation front, inflationary pressures probably continued to heat up in April, mirroring the forward-looking Tokyo CPIs. That would be pleasant news for the Bank of Japan, possibly fueling speculation for policy tightening in the future, perhaps this summer already. The BoJ’s reluctance to tighten policy has devastated the yen, so any hints that this might change can help the currency regain strength. Governor Ueda has signaled he’s open to tightening, provided that inflation is persistent. For the yen, the dream scenario would be for the BoJ to start tightening right as other central banks stop, during a period of turbulence in global markets.Risk-linked currencies eyed, Turkey goes to electionsTurning to currencies with strong links to risk sentiment, the British pound will be in the spotlight Tuesday with the release of jobs data for March. The Bank of England disappointed traders this week by not providing any strong clues about future action, so markets are pricing the rate decision next month almost like a coin toss. In Australia, there’s a barrage of releases starting on Tuesday with the minutes of the latest RBA meeting, where the central bank unexpectedly raised interest rates. The wage price index for Q1 will follow Wednesday, ahead of jobs numbers for April on Thursday. Over in Canada, the latest inflation stats are out Tuesday, ahead of retail sales on Friday. Market pricing suggests the Bank of Canada is done raising rates, so anything that challenges this perception could inject more volatility into the Canadian dollar, which has been shaken around lately by massive swings in oil prices. Finally in Turkey, the nation will elect its next parliament and president on Sunday. President Erdogan is lagging behind his main rival Kilicdaroglu, although neither candidate is expected to secure 50% of the votes, which means there will probably be a second round in two weeks. A strong showing by Kilicdaroglu could help the Turkish lira to appreciate, perhaps with a large gap at the open on Monday, on expectations that a new government will restore orthodox economic policies and allow the central bank to raise interest rates in order to fight runaway inflation. 免责声明: XM Group仅提供在线交易平台的执行服务和访问权限,并允许个人查看和/或使用网站或网站所提供的内容,但无意进行任何更改或扩展,也不会更改或扩展其服务和访问权限。所有访问和使用权限,将受下列条款与条例约束:(i) 条款与条例;(ii) 风险提示;以及(iii) 完整免责声明。请注意,网站所提供的所有讯息,仅限一般资讯用途。此外,XM所有在线交易平台的内容并不构成,也不能被用于任何未经授权的金融市场交易邀约和/或邀请。金融市场交易对于您的投资资本含有重大风险。

所有在线交易平台所发布的资料,仅适用于教育/资讯类用途,不包含也不应被视为用于金融、投资税或交易相关咨询和建议,或是交易价格纪录,或是任何金融商品或非应邀途径的金融相关优惠的交易邀约或邀请。

本网站上由XM和第三方供应商所提供的所有内容,包括意见、新闻、研究、分析、价格、其他资讯和第三方网站链接,皆保持不变,并作为一般市场评论所提供,而非投资性建议。所有在线交易平台所发布的资料,仅适用于教育/资讯类用途,不包含也不应被视为适用于金融、投资税或交易相关咨询和建议,或是交易价格纪录,或是任何金融商品或非应邀途径的金融相关优惠的交易邀约或邀请。请确保您已阅读并完全理解,XM非独立投资研究提示和风险提示相关资讯,更多详情请点击 这里。